Blog

4 min read

Meet the TurboTeam: Goran Maksimovic

And then you realize that the people are your source that you’re learning from. And the people keep you in company and...

Every landlord has their unique story and reasons for buying and renting out property. But beyond things like providing for their eventual retirement and providing someone a great place to live, the primary reason that any real estate investor rents out their property is to generate rental income.

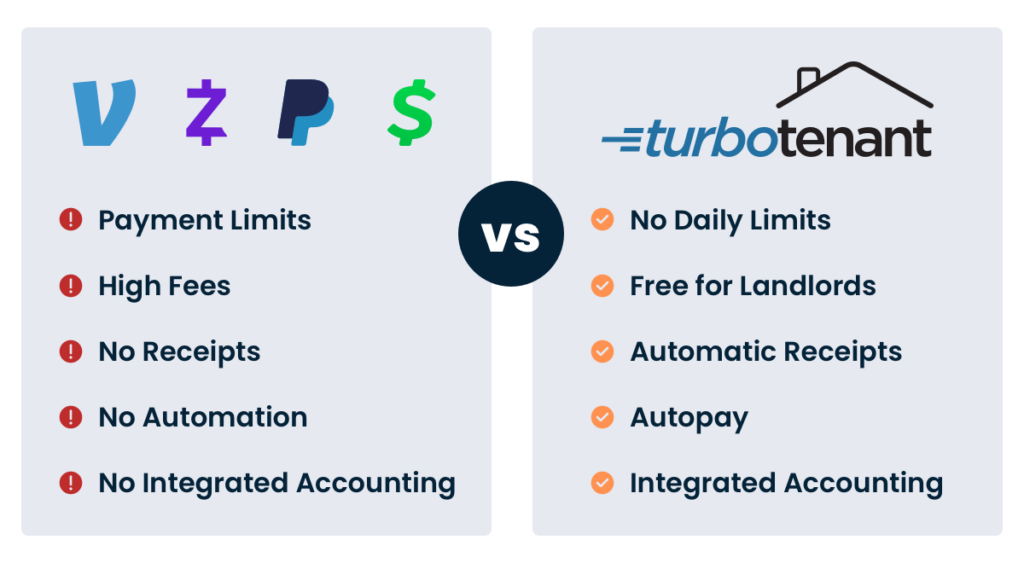

There are many methods for accepting rent payments, and each one comes with its own pros and cons. Here, we’ll break down the risks that your rental business may face when you accept rent with Zelle, Venmo, cash, or checks.

Zelle markets itself as the best method for sending money to friends and family, and you may have tenants wanting to use it to send you monthly rent payments. Zelle works directly with banks, so its functionality depends on whether your bank (or your tenant’s) accepts Zelle.

If they do accept Zelle, each bank will still have limits on daily and monthly payments. These limits may be as low as $1,000 a day and $5,000 per month. If a tenant’s bank does not accept Zelle, then the limits are even more stringent, with a weekly send limit of just $500. According to a recent Apartment List report, the median rent in America is $1379 per month, so Zelle’s payment limits will definitely complicate your ability to collect.

Beyond the limits, Zelle is also risky for rent collection due to the potential for your tenant to accidentally pay the wrong person. Zelle payments are not easily trackable for your business, and partial payments go through instantly, which could halt a nonpayment eviction from proceeding with just a $1 payment. Zelle is also rife with scams that you have to look out for.

Venmo is the ubiquitous payment app that everyone uses to split pizza with friends, but how does it do as a rent collection service? There are a number of issues with Venmo, and one of the biggest is that Venmo charges a 1.9% business fee for every transaction.

If you charge the median rent of $1379, that amounts to $26 every month that’s coming out of your bottom line. Furthermore, Venmo charges consumers an additional 3% fee to send money using a credit card, which will surely ruffle your tenant’s feathers.

Venmo does make it easy to pull tax forms, but instant transfers cost extra with a maximum fee of $15. Just like Zelle, Venmo also has the risk of a tenant accidentally paying the wrong person, and they don’t block partial payments, which may complicate eviction proceedings. Venmo does not allow any recurring payment option, so your tenant will have to put in a new payment every month, which may lead to late payments. Since Venmo is an all-purpose payment app and isn’t tailored for property management, it lacks useful rental features like automatic late fee calculation, which could create more admin work for you.

Another noteworthy downside to Venmo is that it’s impossible to cancel a Venmo payment. Their policies don’t allow a refund to the renter if the tenant pays the wrong amount. In the unlikely event that Venmo chooses to get involved in a payment dispute, they usually side with the buyer, which in your case could take more money out of your pocket.

You may have read the risks of Venmo and Zelle and thought to yourself that this all feels overly complicated. If the goal is to collect rent, then why not resort to the tried and true method of cold hard cash? Cash doesn’t include any extra fees, banks won’t bat an eye at depositing it immediately, and if your tenant can’t afford rent then it’s extraordinarily obvious since they also can’t deliver the right amount of cash.

On the flip side, cash definitely carries its own risks for rent payments. The most obvious problem is that you have to physically collect cash, which can be time consuming and complicated, especially if you’re managing out-of-state rentals. Cash is easy to misplace and can be hard to properly document. Say, for instance, that a payment is a few bills short but the tenant insists they paid in full. How do you prove it?

There are fantastic platforms to streamline your rental management, and if you’ve digitized all the other parts of your rental process (marketing, screening, leases, etc), then why still require cash payments?

Checks carry many of the same risks as cash. If it’s easy to misplace a stack of cash, then it’s even easier to lose a single check – or for your tenant to insist they sent the check but it got “lost in the mail” without any proof. Another important thing to keep in mind is that checks are not used much anymore, and tenants under 40 may not even have a checkbook or be particularly comfortable with writing and delivering a check every month.

Another serious risk to accepting rent via check is that checks can bounce, and it takes a while for you to even know that it bounced. This causes you extra money and time, and especially if you have multiple rental units then this can become a serious headache. Checks can also be canceled by tenants, and there’s no automated way for you to give your tenant a receipt for their payment each month.

Now that we’ve pointed out the flaws of some of the most common payment methods, allow us to point you to the best option.

TurboTenant’s rent payment features are custom made for landlords. We make it easy for landlords and tenants alike to connect their bank accounts, and renters are also able to pay by credit card. We include customizable late fees, and tenants are able to set up automatic rent payments.

All payments are documented in your account, and our support team is available 7 days a week to troubleshoot any issues that you or your tenant may face.

4 min read

And then you realize that the people are your source that you’re learning from. And the people keep you in company and...

5 min read

We have this really good integration. We make them feel like they are part of the company....but it’s like we also make...

4 min read

Well, I guess the thing that pops into my mind right now is you have a lot of freedom to do things...